A complete guide to securities class action lawsuits covering how they work, key legal concepts, timelines, settlement processes, and what investors should expect when participating.

Learn about securities lawsuits tied to your portfolio and recover money!

When corporations mislead investors about their financial health, individual shareholders often face a frustrating reality: their losses may be significant personally, but too small to justify the enormous expense of individual litigation. Securities class action lawsuits solve this problem by allowing affected investors to combine their claims into one powerful legal action.

For retail investors navigating today's complex markets, understanding how class action lawsuits work is essential, not just for potential recovery when things go wrong, but for recognizing the warning signs of corporate misconduct before it impacts your portfolio. This guide breaks down the mechanics, the class action timeline, the class action settlement process, and the key benefits of joining a class action that every investor should understand.

What Are Securities Class Action Lawsuits?

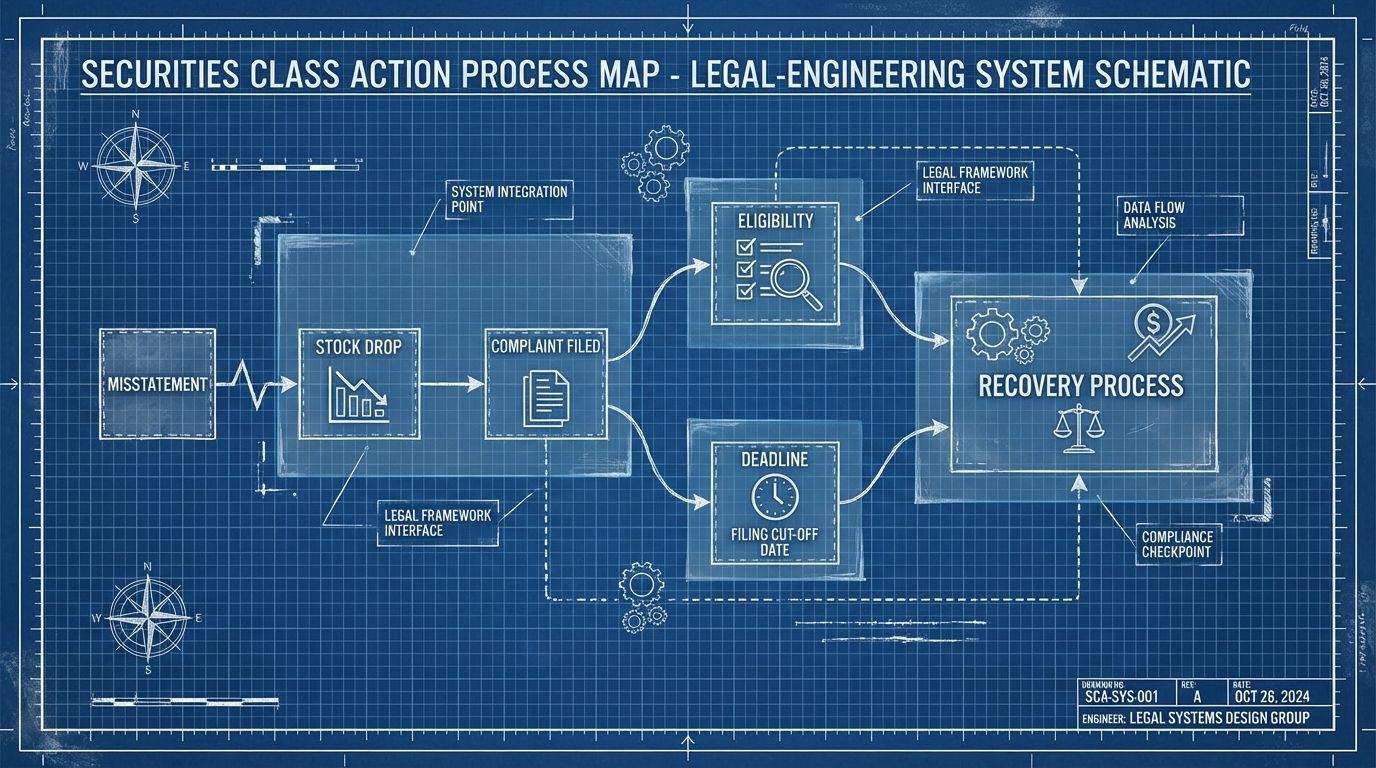

Securities class action lawsuits allow multiple investors who suffered losses from the same corporate misconduct to sue collectively rather than filing thousands of individual cases. Operating under Rule 23 of the Federal Rules of Civil Procedure, these lawsuits aggregate claims from numerous shareholders into a single proceeding led by class representatives on behalf of all similarly affected investors. The class period, the timeframe during which the alleged fraud occurred, determines who qualifies as a class member eligible for potential recovery.

The practical advantage is straightforward: an investor with $5,000 in losses cannot rationally pursue individual litigation that might cost $50,000 in legal fees. Class actions solve this problem by pooling resources across all affected investors, spreading legal costs among participants, and attracting experienced securities attorneys who work on a contingency basis. This transforms economically impractical individual claims into substantial collective cases that defendants must take seriously.

Most securities class actions arise from financial misrepresentation-misleading disclosures about earnings, revenue, or liabilities that artificially inflate stock prices. Data shows that in 2025, 83% of accounting case settlements included allegations of GAAP violations. When the facts emerge through corrective disclosures, stock prices typically collapse, triggering investor losses and potential litigation. Other triggers include regulatory violations such as false SEC filings, inadequate accounting controls, or insider trading, accounting for approximately 13% of recent filings.

Key Mechanics Of Securities Class Action Lawsuits

Securities class actions often arise following stock price declines associated with alleged corrective disclosures that contradict previous corporate statements. Law firms specializing in securities litigation investigate potential claims, often filing complaints shortly after the stock drops. Multiple law firms may file competing complaints for the same alleged fraud, leading courts to consolidate these cases and appoint lead plaintiffs to represent the class, usually institutional investors with the largest financial losses.

The legal foundation rests primarily on Rule 10b-5, which prohibits material false statements or omissions that deceive investors. Plaintiffs must demonstrate that defendants made misleading public statements, that these statements were material to investment decisions, that investors relied on the integrity of the market price, and that the misrepresentations caused measurable financial losses when corrected including that defendants acted with scienter (intent or recklessness).

Named defendants typically include the company itself, key executives like the CEO and CFO who made or approved misleading statements, and sometimes auditors or underwriters who facilitated the fraud. The complaint alleges these parties engaged in practices, such as accounting irregularities, misleading guidance, or concealed risks, that artificially inflated stock prices until the truth emerged.

What to Expect From The Class Action Timeline

Securities class action lawsuits follow a predictable multi-year timeline. The process begins with case filing and consolidation, typically within weeks or months of the corrective disclosure. Courts then appoint lead plaintiffs and approve lead counsel, usually within 60-90 days of the initial filing.

The discovery phase follows, during which both sides exchange documents and take depositions. This phase often lasts 12-24 months and involves an extensive review of internal company communications, financial records, and witness testimony. During discovery, defendants typically file motions to dismiss, arguing the complaint fails to meet legal standards. Courts may take 6-12 months to rule on these motions.

If the case survives dismissal, the parties often enter into settlement negotiations, though some cases proceed to class certification hearings, where courts formally determine whether the case meets Rule 23 requirements for class treatment. Settlement discussions may occur at any point but frequently intensify after discovery reveals damaging evidence or courts deny dismissal motions.

Most securities class actions settle rather than proceeding to trial. From initial filing to final settlement approval, the typical timeline spans 2-4 years, though complex cases may take longer.

The Class Action Settlement Process Explained

When parties reach a settlement agreement, the process requires court approval to ensure fairness to all class members. The court first grants preliminary approval, after which notice is sent to all potential class members informing them of the settlement terms, their options to participate or opt out, and the date of a fairness hearing.

Class members have several options during this period. Most do nothing and remain automatically included, ultimately receiving their proportional share of the settlement. Investors who wish to opt out must submit their requests by the specified deadline, preserving their right to pursue individual litigation. Class members may also object to the settlement terms by submitting written objections or appearing at the fairness hearing.

At the fairness hearing, the court evaluates whether the settlement is fair, reasonable, and adequate for class members. Judges consider factors such as the strength of the plaintiffs' case, the amount of recovery relative to potential damages, the risks of continued litigation, and whether class members support the settlement. After hearing objections and reviewing submissions, the court issues final approval or rejection.

Upon final approval, the settlement administrator distributes funds to eligible class members who submit valid claims forms documenting their losses during the class period. Settlement amounts vary widely, from millions to hundreds of millions of dollars, but individual recoveries typically represent only a fraction of actual losses after legal fees, administrative costs, and distribution among all claimants.

While not a securities fraud case, the 2023 stock loan antitrust settlement against JPMorgan, Morgan Stanley, Goldman Sachs, UBS, and EquiLend demonstrates the potential scale of these recoveries. The combined $581 million settlement not only provided monetary compensation but also mandated governance reforms through an antitrust code of conduct, showing how class actions can achieve both financial recovery and systemic changes.

Benefits of Joining a Class Action for Investors

One of the most significant benefits of joining a class action is access to justice that would otherwise be economically impossible. By pooling resources, investors transform individually small claims into collectively significant cases that attract top securities attorneys working on a contingency basis, meaning no upfront legal fees.

Class actions also provide leverage against well-funded corporate defendants who might otherwise outlast individual plaintiffs through expensive procedural battles. The collective nature creates economies of scale in litigation costs, expert witnesses, and discovery expenses that no individual investor could afford.

Additionally, class members benefit from professional legal representation without having to be actively involved. Lead plaintiffs and their counsel handle the litigation while class members simply await the outcome. For busy retail investors, this passive participation requires minimal time commitment, aside from submitting a claims form if a settlement occurs.

What Investors Need to Know About Participation

Participation in securities class actions typically occurs after a court certifies a class. At that stage, investors who fall within the class definition are generally included as class members unless they choose to opt out. While no action is usually required to remain in the class, investors must submit a valid claim form and supporting documentation to receive any recovery.

To obtain settlement proceeds, investors are required to document their transactions and losses. These forms require proof of purchase, such as brokerage statements showing when you bought shares, how many you purchased, at what price, and when you sold (if applicable). Because claims are subject to strict deadlines, failing to submit a timely and complete claim may result in the loss of any recovery.

Investors should watch for class action notices, which settlement administrators mail to registered shareholders and publish in financial media. You can also monitor securities class action websites and databases that track active cases and settlement opportunities.

Understanding the trade-offs is important. By remaining in the class, you accept the settlement amount determined through negotiation and court approval, which may be substantially less than your actual losses. You also release defendants from future claims related to the same conduct. Opting out preserves your right to sue individually but requires you to fund your own litigation, an expensive proposition that makes sense only for investors with substantial losses.

Making the Decision: Is Joining Right for You?

For most retail investors, remaining in the class action makes practical sense. The automatic inclusion requires no upfront investment, no ongoing involvement, and no financial risk beyond the losses already suffered. While settlement recoveries rarely make investors whole, receiving a partial recovery through the class action beats receiving nothing from individual litigation you cannot afford to pursue.

Before making a decision, consult a securities attorney to evaluate the situation and provide guidance. Securities class action lawsuits serve an important function in holding corporations accountable when they mislead investors. While the process is lengthy and recoveries are often modest relative to actual losses, these lawsuits provide retail investors access to justice they could never achieve individually. Understanding how class action lawsuits work, what to expect from the class action timeline, how the class action settlement process unfolds, and the benefits of joining a class action empowers you to make informed decisions when corporate misconduct affects your investments.

Disclaimer: The information provided in this article is for informational and educational purposes only and does not constitute legal or investment advice. Readers should conduct their own research and consult with qualified professionals before making any investment decisions or taking legal action. This information is provided to help identify potential risks. Always review and verify risks before taking investment action.