Kyndryl Holdings, Inc. (KD) Securities Class Action Lawsuit Update

Kyndryl Holdings (KD) Securities Class Action: Internal Controls, Cash Flow Reporting, and a 55% Stock Collapse

BellRing Brands faces a securities class action

Learn about securities lawsuits tied to your portfolio and recover money!

BellRing Brands, Inc. did not lose investor confidence overnight. According to a newly filed securities class action complaint, the erosion came in stages—first masked by inventory dynamics, then exposed by disclosures that revealed a more fragile demand picture beneath the surface.

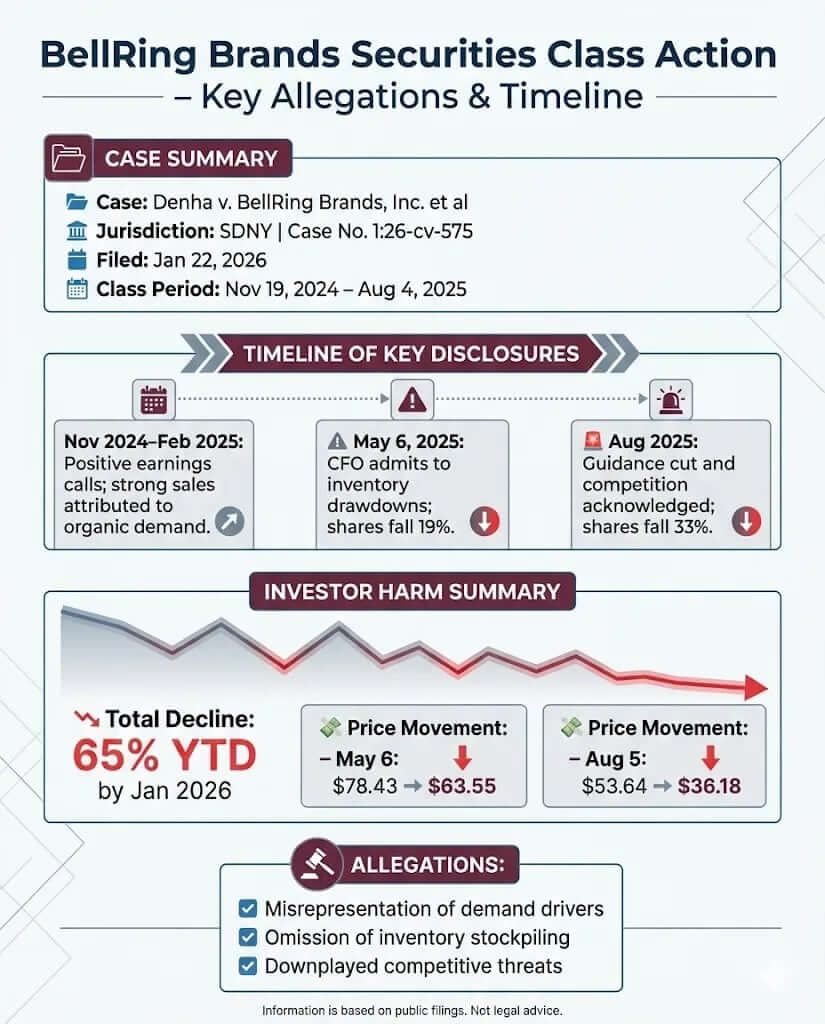

In January 2026, an investor lawsuit was filed in the Southern District of New York alleging that BellRing and two senior executives misled the market about the sustainability and drivers of the company’s sales growth. Investors allege that what appeared to be organic momentum was, in fact, temporary retailer stockpiling that concealed competitive pressure and weakening end-consumer demand. When that reality emerged, the stock fell sharply—twice.

“Most BRBR shareholders never file or join the class action, which means they miss out on potential recovery funds,” said Attorney Joe Levi.

BellRing Brands is a consumer packaged goods company focused on what it calls “convenient nutrition,” with ready-to-drink protein shakes, powders, and bars sold primarily under the Premier Protein brand. That brand alone accounts for approximately 85% of company revenue.

The company operates an asset-light model, relying on third-party manufacturers while distributing through club stores, grocery chains, mass retailers, pharmacies, and e-commerce channels. For years, BellRing’s growth narrative was shaped by supply constraints. Demand routinely outpaced manufacturing capacity, limiting the company’s ability to meet retailer orders.

In early 2024, that constraint eased. BellRing expanded third-party manufacturing capacity, including new facilities largely dedicated to its products. Management told investors this inflection allowed the company to pivot—from simply filling orders to actively driving demand through promotions, distribution gains, and marketing initiatives. That shift framed everything that followed.

Throughout the class period, BellRing executives repeatedly attributed sales growth to organic demand, promotional success, and macro tailwinds around protein consumption.

In November 2024, CEO Darcy Horn Davenport told investors that “momentum remains high” and that the company’s brands “deeply resonate with consumers,” citing organic growth, distribution gains, and demand drivers layered in for the first time in years. CFO Paul Rode emphasized volume growth, stating that Premier Protein sales increases were driven by “organic growth and distribution gains.”

At the same time, management downplayed competition. When asked directly about evolving competitive dynamics in early 2025, Davenport said there were “not a ton of major changes” and described the ready-to-drink category as having a “competitive moat” because it was “highly complex” and “hard to formulate.”

According to the complaint, those representations omitted a critical fact: reported sales were materially inflated by retailer inventory stockpiling. Customers, still scarred by years of shortages, allegedly over-ordered to protect shelf availability. That behavior boosted shipments without reflecting true end-consumer demand. Once confidence in supply returned, retailers began cutting back—revealing weaker underlying momentum and intensifying competition that management had previously minimized.

The alleged misstatements began on November 19, 2024, when BellRing reported strong fiscal 2024 results and framed growth as demand-driven. Similar messaging continued through the February 2025 earnings cycle, with executives touting accelerating momentum and dismissing competitive threats.

The narrative cracked on May 6, 2025. During an earnings call, CFO Rode disclosed that several key retailers had lowered their weeks of supply on hand, creating a mid-single-digit headwind to upcoming growth. Davenport acknowledged that retailers had been “hoarding inventory” after capacity constraints and were now drawing it down—but insisted there was “no softness, no concern around consumption.”

The market disagreed. BellRing shares fell $14.88, or 19%, in a single day.

The second break came in August 2025. After narrowing full-year sales guidance, Davenport openly attributed the slowdown to competition, noting that new protein RTDs had entered the category and that rival brands had gained shelf space alongside BellRing at major club retailers. The following day, the stock fell another $17.46, or nearly 33%.

The complaint ties investor losses directly to these disclosures. On May 6, 2025, BellRing stock dropped from $78.43 to $63.55 on unusually heavy trading volume. Three months later, after competitive pressures were acknowledged, shares fell from $53.64 to $36.18 in a single session.

Plaintiffs allege that investors who purchased shares during the class period paid artificially inflated prices—inflation sustained by representations that obscured the true drivers of reported growth. When inventory dynamics and competitive realities surfaced, that inflation collapsed, wiping out billions in market value.

The lawsuit is pending in the U.S. District Court for the Southern District of New York.

The complaint asserts claims under Sections 10(b) and 20(a) of the Securities Exchange Act and Rule 10b-5 against BellRing, CEO Davenport, and CFO Rode. Investors allege a scheme to misrepresent demand sustainability, omit material facts about inventory stockpiling, and minimize competitive pressure.

Scienter allegations focus on management’s admissions that they knew retailers had been hoarding inventory and that increased competition was not surprising—facts plaintiffs say were withheld while bullish narratives were repeated. The case is in its earliest stages, with no motion practice yet resolved.

Investor confidence in BellRing Brands has eroded significantly following a series of disclosures that contradicted the company's growth narrative. By January 2026, the stock had hit a 52-week low of $22.45, reflecting a staggering 65% decline year-to-date. Financial outlets have characterized the market reaction as severe, noting that investor anxiety regarding near-term profitability and competitive pressures has outweighed previous optimism.

The volatility was punctuated by sharp sell-offs, including a 19% drop in May 2025 and a 33% collapse in August 2025, which signaled to the market that the company's reported demand drivers were disconnected from operational reality.

Wall Street's stance on BellRing has shifted from bullishness to caution as operational cracks emerged. BofA Securities downgraded the stock from "Buy" to "Neutral" and slashed their price target, citing "soft results" and an "intensifying competitive backdrop". They noted that consumption data was decelerating, suggesting potential market share losses ahead.

Seeking Alpha contributors described the outlook as tough to be bullish in the near term, highlighting that the company had issued downside guidance that missed consensus estimates.

Market analysts have also scrutinized the disconnect between "shipments" and "consumption," with reports noting that analysts questioned why consumption wasn't higher given the reported destocking, directly challenging management's explanations during the turbulent earnings calls.

The alleged misstatements were made across Form 10-Ks, 10-Qs, Form 8-Ks, press releases, and earnings calls. BellRing reported revenue based on shipments when control passed to customers—a policy that, while compliant with accounting standards, made results particularly sensitive to inventory behavior.

Plaintiffs argue that risk disclosures failed to adequately warn investors that reported growth could be driven by temporary retailer stockpiling rather than sustainable consumer demand, or that intensifying competition could materially weaken sales once inventory normalized.

The BellRing case is not just about protein shakes. It is about optics—how growth is measured, explained, and sold to the market. When shipment-based revenue masks inventory dynamics, confidence can rest on fragile ground.

For investors, the lawsuit is a reminder to scrutinize the difference between consumption and shipments, to listen carefully when analysts probe inconsistencies, and to treat claims of “competitive moats” with caution in fast-crowding categories. The market eventually forces clarity. When it does, it rarely does so gently.

How to Join the BellRing Brands (BRBR) Class Action

Disclaimer: This shareholder alert is for informational purposes only and does not constitute legal advice. Consult a qualified attorney for personalized guidance. No specific outcomes are guaranteed.

Kyndryl Holdings (KD) Securities Class Action: Internal Controls, Cash Flow Reporting, and a 55% Stock Collapse

A practical guide explaining securities fraud, how it works, key warning signs, real-world examples, and actionable steps investors can take to avoid and report fraud.

![Lakeland Industries, Inc. [LAKE] Securities Class Action Lawsuit Update](https://media.suewallst.com/cms-dev/LAKE_c3a50beb70.png)

Lakeland Industries, Inc. (LAKE) Lawsuit: Acquisition Strategy Unravels Under Pressure